Annuities provide retirement income you can count on.

Annuities provide retirement income you can count on. They are designed to help convert a portion of your savings into a predictable stream of income that can last for years — or even for life. Unlike investments that fluctuate with the market, many annuities offer principal protection and contractual guarantees. This can help reduce uncertainty and bring stability to your overall retirement strategy. Whether you’re nearing retirement or already there, annuities can play a key role in building long-term financial confidence.

An annuity is a retirement-focused financial product that can provide several valuable benefits, including:

Tax-deferred growth

Earnings inside the annuity accumulate without being taxed each year. Taxes are typically due only when funds are withdrawn, allowing your money the opportunity to compound over time similar to a 401(k).*

guaranteed lifetime income

Annuities can be structured to deliver a reliable income stream for a specific number of years or for the remainder of your life. This can help create stability and predictability in retirement.

guaranteed death benefit

If you pass away, the remaining value in your annuity can be paid directly to your named beneficiaries. This may help them receive the funds more efficiently and potentially avoid the probate process.

*Annuity payments from a tax-qualified plan will be fully taxable as ordinary income. Withdrawals made prior to age 59 1/2 may be subject to an additional 10% IRS tax penalty.

understanding retirement annuities

Retirement annuities provide a way to grow your savings based on your personal risk comfort level while allowing earnings to accumulate on a tax-deferred basis. When you’re ready to retire, they can be structured to create a dependable income stream that lasts for a specific period — or even for the rest of your life.

Annuities can begin paying income immediately or be set up to provide income at a future date. Payments may be taken as a lump sum or distributed over time, depending on your needs and retirement strategy.

Different types of annuities serve different purposes, and understanding how each works can help you choose the right fit for your long-term goals.

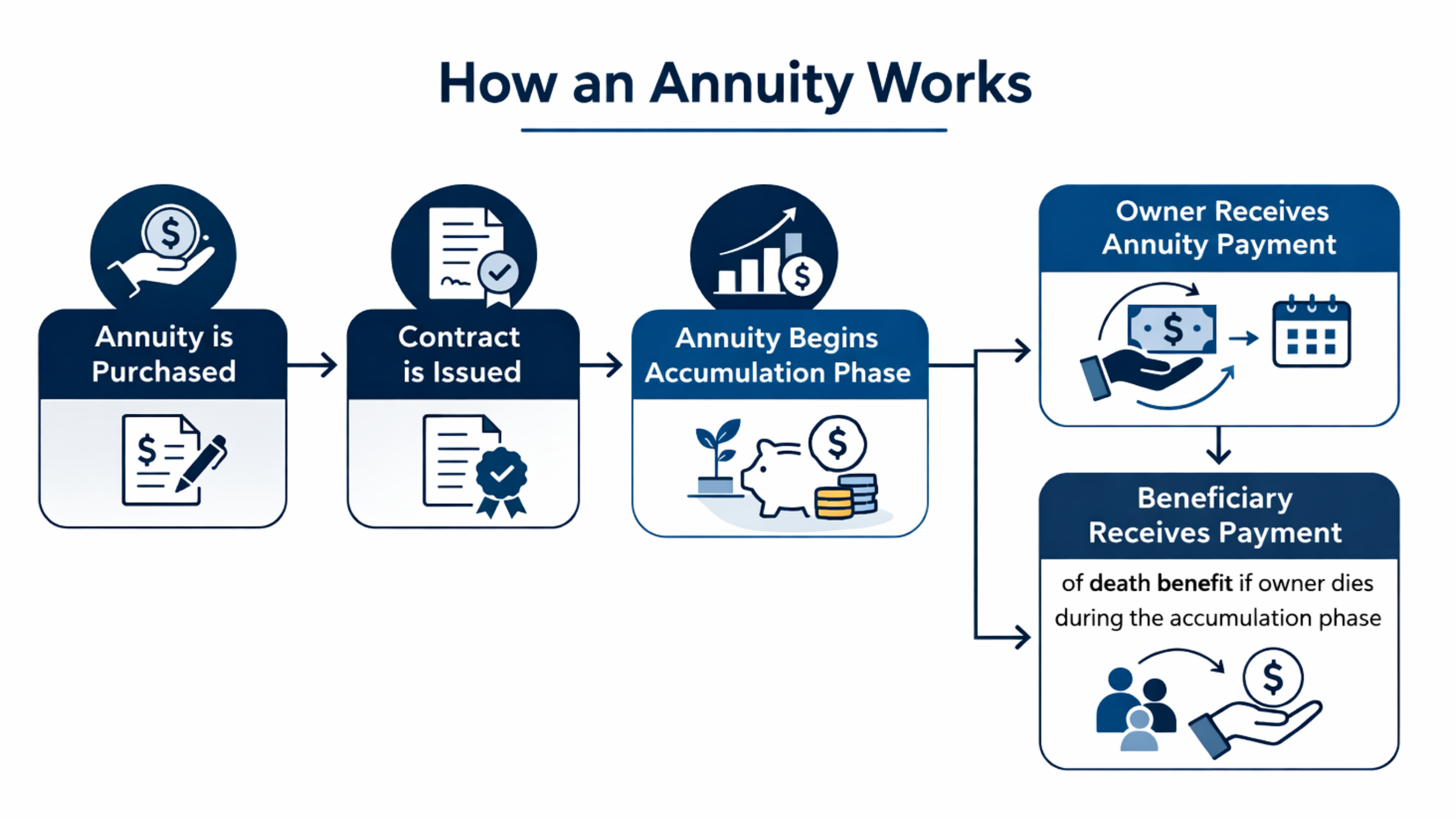

An annuity is simply a contract between you and an insurance company designed to help grow your money and provide income in retirement.

Annuities typically have 2 phases:

1. Accumulation Phase

This is the growth stage. During this period, you fund the annuity either with a lump sum or ongoing contributions, and your money grows tax-deferred. Depending on the type of annuity, growth may be based on a fixed rate, an index strategy, or other crediting method.

2. Distribution (Income) Phase

This is when you begin receiving payments from the annuity. You can structure income to last for a specific number of years or for the rest of your life. The goal during this phase is to create predictable, reliable income to support your retirement needs.

Accumulation

Distribution

immediate annuities and deferred annuities

Funded with a single lump-sum purchase

Can provide a guaranteed lifetime stream of income

Referred to as single premium immediate annuities, or SPIAs

Immediate Annuities

Funded with either a lump sum payment or a series of payments

Pay out at a future date

Divided into three categories: Fixed, Indexed and Variable

Deferred Annuities

types of deferred annuities:

fixed annuities

Fixed annuities offer a guaranteed interest rate for a set period of time. Your principal is protected, and growth is predictable. They are designed for conservative investors who prioritize stability over market-based growth.

indexed annuities

Indexed annuities link growth to a market index, such as the S&P 500, without directly investing in the market. They offer downside protection (typically a 0% floor) while allowing for capped or participation-based upside potential. They are often used for balanced growth with protection.

variable annuities

Variable annuities invest your money in market-based subaccounts similar to mutual funds. This provides higher growth potential but also exposes your account to market risk and losses. They are best suited for individuals comfortable with market volatility and long-term investment risk.

-

An annuity is a contract between you and an insurance company designed to help grow your money and provide income, typically for retirement. You contribute a lump sum or series of payments, and in return, the company agrees to credit interest and potentially provide future income payments. Growth inside an annuity is tax-deferred until withdrawals are made. Annuities can be structured to provide income for a specific period of time or for the rest of your life. They are commonly used to create predictable, reliable retirement income.

-

An annuity works by allowing you to deposit money with an insurance company, where it grows tax-deferred over time. During the growth period, your funds earn interest based on the type of annuity you choose. When you’re ready, you can begin taking income as a lump sum or as scheduled payments. Some annuities can provide income for a set number of years or even for the rest of your life. It’s designed to help turn your savings into predictable retirement income.

-

How much an annuity pays each month depends on several factors, including how much you invest, your age, the type of annuity, and when you start income. The larger the amount funded and the later you begin payments, the higher the monthly payout may be. If structured for lifetime income, payments are calculated to last as long as you live. Each contract is customized based on your goals and timing.

-

Yes, annuities can be taxable — but it depends on how they’re funded and how withdrawals are taken.

If you use pre-tax (qualified) money, such as funds from a traditional IRA or 401(k), withdrawals are generally fully taxable as ordinary income. If you use after-tax (non-qualified) money, only the earnings portion is taxable — your original contributions are not taxed again.

Taxes are typically owed when you withdraw funds, since growth inside the annuity is tax-deferred.

Get Your Free Retirement Strategy Review

Work with a licensed advisor at Momentum Life Group to build a plan for income, protection, and long-term financial security.

✔ No obligation

✔ No pressure

✔ Customized strategy based on your goals